In the GST filing process, businesses need to file GSTR-1 monthly to report sales, followed by GSTR-3B to report input tax credits (ITC) and make GST payments. When applicable, refunds require the filing of specific forms. File your GST with us.

A. GST Payments

What are GST Payments?

There are three main GST payments based on the type of transaction:

- IGST (Integrated GST): For interstate transactions (paid to the central government)

- CGST (Central GST): For intrastate transactions within the same state (paid to the central government)

- SGST (State GST): For intrastate transactions within the same state (paid to the state government)

| Type of Transaction | CGST | SGST | IGST |

| Goods sold from Jaipur to Gujarat | No | No | Yes |

| Goods sold within Delhi | Yes | Yes | No |

| Goods sold from Mumbai to Pune | Yes | Yes | No |

Other Types of GST Payments

- Tax Deducted at Source (TDS): TDS requires a buyer to deduct tax before paying a supplier. For example, a government agency might deduct 1% TDS on a ₹15 lakh contract before paying the remaining balance.

- Tax Collected at Source (TCS): Generally TCS applies to e-commerce. E-commerce sellers may receive payments after TCS deductions of around 2%.

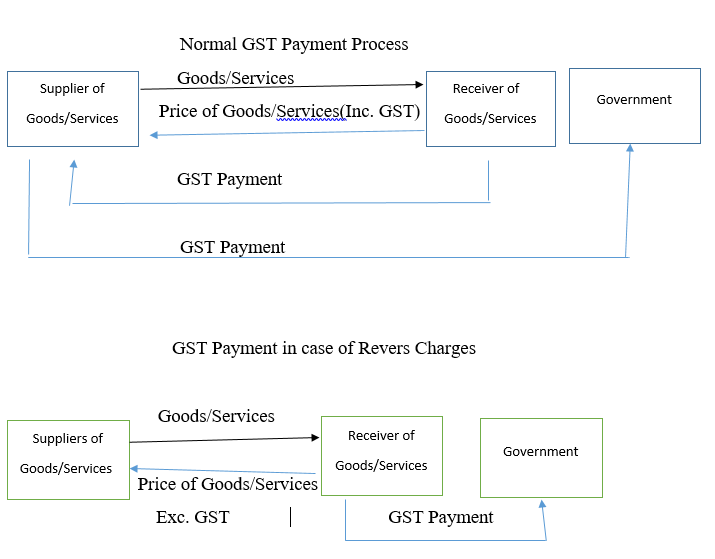

- Reverse Charge Mechanism (RCM): Under RCM, Shifts GST payment responsibility from the supplier to the buyer.

Additional Charges

Payments may also include:

- Interest, Penalties, and Fees: These must be paid in cash and cannot be claimed for ITC.

Calculating GST Payments

To calculate GST payments, subtract ITC from the total tax liability and add any interest or late fees to determine the final payable amount.

Payment for Different Types of Dealers

- Regular Dealers: Calculate GST based on sales, subtracting ITC from tax liability.

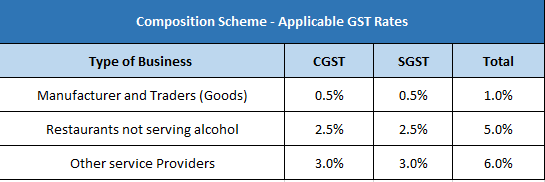

- Composition Dealers: Pay a fixed GST rate on total sales, based on their business type.

Who Should Pay GST?

GST payments must be made by:

- Registered dealers with GST liability.

- Dealers under the Reverse Charge Mechanism (RCM).

- E-commerce operators (for TCS).

- Dealers required to deduct TDS.

When to Pay GST?

GST payments are due with the filing of GSTR-3B, by the 20th of the following month.

B. GST Refunds

What is a GST Refund?

A GST refund arises when tax paid exceeds tax liability. The refund process is standardized and conducted online, with specific time limits for each refund type.

When Can Refunds Be Claimed?

Refunds can be claimed in cases such as:

- Excess tax paid due to errors

- Exports, including deemed exports

- Accumulated ITC when output is tax-exempt or nil-rated

- Purchases made by embassies or UN bodies

- Tax refunds for international tourists

- Finalized provisional assessments

Example of Refund Calculation

If Mr. B’s GST liability for September is ₹50,000 but he mistakenly pays ₹5 lakh, he has overpaid by ₹4.5 lakh and can claim it as a refund. Refund claims should be made within 2 years from the date of payment.

How to Claim a GST Refund?

Refunds must be claimed using Form RFD-01 within two years from the relevant date, which varies by case. The form must also be certified by a Chartered Accountant.

FAQs on GST Payments and Refunds:

• What are the main types of GST payments, and when are they required?

GST payments include IGST (for interstate transactions), CGST, and SGST (both for intrastate transactions). Payments are due when filing GSTR-3B, typically by the 20th of each month.

• What is the Reverse Charge Mechanism (RCM) under GST?

Under RCM, the buyer, rather than the supplier, pays the GST. This applies to specific goods or services as determined by the government.

• When am I eligible to claim a GST refund?

You may claim a refund if you’ve paid excess tax, accumulated ITC due to exempt or nil-rated outputs, or made exports. Refunds also apply to tax paid on purchases by embassies or UN bodies.

• What penalties apply if GST payments are delayed or short-paid?

Late or underpaid GST incurs 18% interest. Additionally, a penalty of either ₹10,000 or 10% of unpaid tax (whichever is higher) may apply.

• How do I calculate the GST payment I owe?

To calculate GST, subtract ITC from your tax liability and add any applicable interest or fees for the final amount due.