An intimation under Section 143(1) is issued by the Income Tax Department after your filed income tax return (ITR) is processed. It includes details such as your ITR acknowledgement number, a complete summary of income particulars as reported in your ITR, and as computed by the department. If there is any discrepancy between the figures filed by you and those calculated by the department, you are required to respond accordingly. The processing of an ITR must be completed within nine months from the end of the financial year in which the return was filed. This article explains the meaning of an intimation under Section 143(1), the cases when it is issued, applicable timelines, and how to respond.

Letter of Intimation u/s 143(1)

An income tax return may be filed voluntarily under Section 139 or in response to a notice issued under Section 142(1). It is important to understand what takes place once a taxpayer files the return of income.

The process by which the Income Tax Department examines the filed return is called an assessment. The department conducts a preliminary assessment of all returns and notifies taxpayers of the outcome. This initial evaluation includes checking for arithmetical mistakes, internal inconsistencies, accuracy of tax computation, and verification of tax payments. The entire preliminary assessment process is automated and managed by the Central Processing Centre (CPC).

After the evaluation, the system automatically issues an intimation under Section 143(1), highlighting any apparent discrepancies or errors detected by the system.

When Does One Receive an Intimation under Section 143(1)?

Every taxpayer receives an intimation under Section 143(1) once their income tax return (ITR) has been successfully processed.

As explained earlier, this is an automated, system-driven process that checks the arithmetical accuracy, validates details available with the department, verifies information declared in the return, and ensures compliance with the provisions of the Income Tax Act. The system then generates a comparison report. This automation significantly reduces the manual involvement of income tax officers.

If a taxpayer has paid excess tax, the intimation will show a tax refund, which is issued only if the refund amount exceeds ₹100. Conversely, if there is a shortfall in tax payment, the intimation will indicate the tax demand along with a challan for payment. Essentially, it serves as an acknowledgment confirming that the ITR filed by the taxpayer aligns with the department’s assessment.

Centralized Processing Centre (CPC)

With the growing number of income tax returns and the challenges of jurisdiction-based processing, the Income Tax Department faced delays in return processing.

To address this, the Finance Act, 2008 authorized the Central Board of Direct Taxes (CBDT) to create a centralized processing system to determine tax payable or refunds more efficiently. Based on the recommendations of the Technical Advisory Group, the department established the Centralized Processing Centre (CPC) in Bengaluru to handle both paper and electronic returns without direct taxpayer interaction and without jurisdictional limitations.

The CPC initiative brought advantages for both taxpayers and the department. For taxpayers, it ensured quicker and smoother preliminary processing of returns. For the department, it automated the initial assessments, allowing officers to focus on more complex cases.

While any communication from the Income Tax Department may seem intimidating, an intimation under Section 143(1) is routine and not a cause for concern. It simply informs taxpayers about the outcome of the system’s preliminary processing of their return.

Preliminary Assessment under Section 143(1)

The initial processing of income tax returns by the Centralized Processing Centre (CPC) is fully automated, and the intimation under Section 143(1) is a computer-generated document. The CPC cross-verifies the data submitted in each tax return with information available in the department’s records, such as Form 26AS, TDS statements, and details provided by collecting banks. This intimation generally highlights any apparent discrepancies identified by the automated system.

Once a return is filed, the computerized system recalculates the total income or loss based on departmental records and compares it with the data submitted by the taxpayer. The intimation includes two columns — ‘As provided by the taxpayer in the Return of Income’ and ‘As computed under Section 143(1)’.

The comparison covers key components such as:

- Income under various heads

- Gross total income

- Deductions under Chapter VIA (like Sections 80C, 80D, etc.)

- TDS, advance tax, and self-assessment tax paid

Necessary adjustments are made to determine the final tax liability or refund. Before making such adjustments, the taxpayer is notified electronically (via the registered email ID) about the proposed changes. Any response received within 30 days of the intimation date is considered; otherwise, the adjustments are finalized as computed. The final liability is then adjusted against TDS, advance tax, or relief under Sections 90/91, and the intimation is issued to the taxpayer.

Types of Intimations under Section 143(1):

- Intimation with no demand or refund: Issued when the return is accepted as filed without any adjustments.

- Intimation determining demand: Sent when discrepancies lead to additional tax liability.

- Intimation determining refund: Issued when excess tax is found refundable, either as filed or after making necessary adjustments.

In cases where a demand arises, a notice for payment is issued, whereas refunds are credited to the taxpayer’s account.

Nature of Adjustments under Section 143(1):

The computation of total income or loss under Section 143(1) may involve adjustments for:

- Arithmetical errors in the return

- Incorrect claims apparent from the return, such as:

- Inconsistent entries (e.g., income deducted from one head but not disclosed under another)

- Disallowance of set-off of losses carried forward from returns filed after the due date

- Disallowance of expenses mentioned in the audit report but not reflected in the ITR

- Inconsistent entries (e.g., income deducted from one head but not disclosed under another)

Time Limit for Issuing Intimation under Section 143(1):

An intimation under Section 143(1) must be issued within nine months from the end of the financial year in which the return is filed. For instance, if a return for FY 2023–24 is filed in July 2024, the intimation may be sent any time up to 31st December 2025.

If no intimation is received within this period, it indicates that no adjustments were made, and the return acknowledgment itself is deemed to be the intimation under Section 143(1).

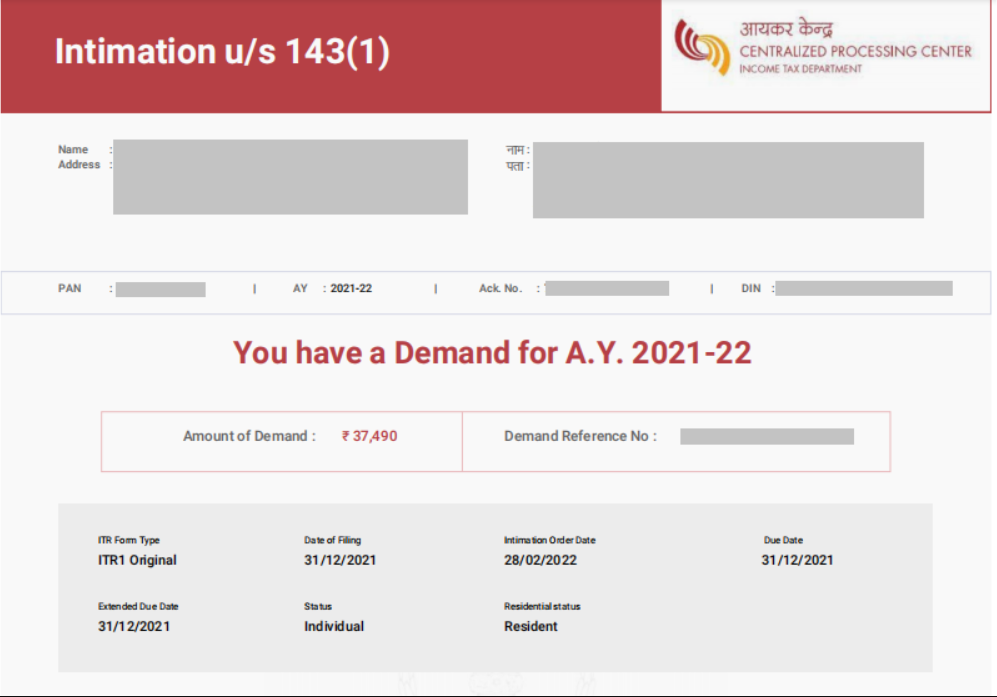

Sample of an Intimation under Section 143(1)

What is the Password for Intimation under Section 143(1)?

The intimation issued under Section 143(1) is sent as a password-protected document. To open the file, you need to use your PAN (in lowercase) followed by your date of birth in the DDMMYYYY format, without any spaces.

Example:

If your PAN is ABCDE1234E and your date of birth is 01/01/2000, then the password to open your intimation file will be:

abcde1234e01012000

Action to be Taken by the Taxpayer after Receiving an Intimation under Section 143(1)

Upon receiving an intimation under Section 143(1), the first step is to carefully review the document to ensure it pertains to your own return and the financial year mentioned is correct. Verify essential details such as your name, PAN, address, assessment year, and e-filing acknowledgment number to confirm accuracy.

If you identify any genuine errors made while filing your return and they can be corrected, you may file a revised return through the income tax e-filing portal.

However, if you believe no errors were made and disagree with the adjustments made by the CPC or automated system, you can file a rectification application under Section 154(1) to report and correct the mistake reflected in the intimation. You should also submit your response online on the e-filing portal indicating whether you agree or disagree with any tax demand raised.

If you are dissatisfied with the processing of your rectification request, you can raise an online grievance or contact your Assessing Officer. If the issue remains unresolved, a complaint may be filed with the Income Tax Ombudsman.

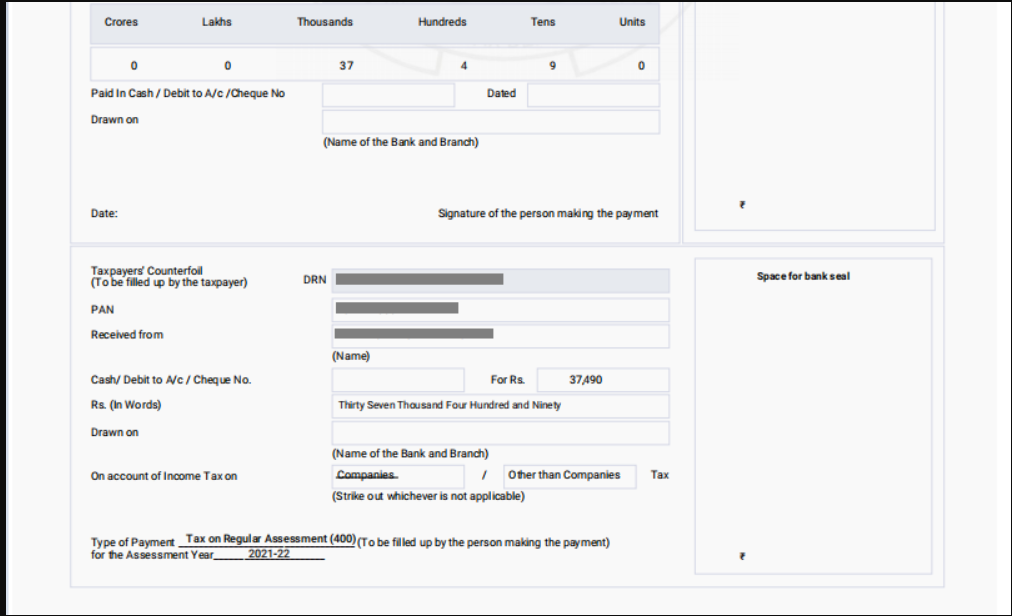

In cases where you agree with the tax demand raised after adjustments, you must pay the tax due accordingly. While making payment through the OLTAS challan, select “Tax on regular assessment (400)” under the Type of Payment section. If you prefer to pay the tax physically, a pre-filled challan will be attached to your intimation for convenience.

FAQs on Intimation under Section 143(1)

1. I received a demand notice under Section 143(1) for ₹5,000. What should I do?

First, verify the reason for the tax demand shown in the intimation. If you agree with it, you must pay the tax amount using a challan. While making the payment, select “Tax on regular assessment (400)” under the Type of Payment category. If you disagree with the demand, submit your response online through the income tax portal explaining your position.

2. What if I disagree with the refund mentioned in the intimation order?

If the refund calculated by the CPC in your intimation order is lower than expected, you may either file a revised return or a rectification request. A revised return should be filed if you made an error while filing your original return, whereas a rectification request can be made when you identify an error in the CPC’s processing.

3. What causes the difference in TDS as per the taxpayer and as computed under Section 143(1)?

A mismatch in TDS may occur if the TDS details reflected in Form 26AS or AIS differ from the TDS claimed in your ITR. If you believe your TDS claim is correct, file an online rectification application under Section 154(1) to correct the discrepancy in the intimation order.

4. How can I file a rectification for an intimation under Section 143(1)?

To file a rectification, log in to the income tax e-filing portal, go to ‘My Account’ → ‘Rectification’, fill in the required details, upload any necessary documents, and submit the request online.

5. What if I don’t receive my intimation under Section 143(1) within the specified period?

If you do not receive any intimation within the prescribed time, the acknowledgment of your return will be treated as the intimation itself, provided there is no tax payable or refund due, and no adjustments have been made by the department.

6. What is the password for the intimation received under Section 143(1)?

The intimation file sent by the Income Tax Department is password-protected. To open it, enter your PAN (in lowercase) followed by your date of birth in DDMMYYYY format, without any spaces.

Example: If your PAN is ABCDE1234E and date of birth is 01/01/2000, your password will be abcde1234e01012000.

7. What if I haven’t received an intimation order even after one year from the relevant assessment year?

If no intimation has been received even after one year, it means that there is no outstanding tax liability or refund due, and your filed ITR is deemed to be the final intimation under Section 143(1).

8. Can an intimation under Section 143(1) be revised later?

Yes, if you identify any mistakes in your filed return, you can file a revised return before the end of the relevant assessment year or before the assessment is completed, whichever is earlier.

9. Will I be penalized if I ignore an intimation under Section 143(1)?

Ignoring an intimation that reflects a tax demand may lead to further action, including notices under Section 156 for tax recovery and possible interest or penalties. It is always advisable to review and respond promptly.

10. How will I receive the intimation under Section 143(1)?

The intimation is sent electronically to your registered email ID and also made available in your income tax e-filing account under the ‘View e-Filed Returns/Forms’ section.

11. How long does it take to receive a refund after processing under Section 143(1)?

Once your return is processed and a refund is determined, it is generally credited to your registered bank account within a few weeks, depending on the CPC’s processing schedule.

12. What if I disagree with both the tax demand and adjustments made under Section 143(1)?

You can file a rectification request under Section 154(1) or submit a grievance online through the e-filing portal. If the issue persists, contact your Assessing Officer or escalate the matter to the Income Tax Ombudsman.