Section 17(5) of the CGST Act, commonly known as the “blocked credit” provision, is a crucial clause for every regular GST-registered taxpayer. It outlines specific transactions where GST is paid, but the Input Tax Credit (ITC) cannot be claimed by the business. This section highlights the categories of ineligible ITC in a detailed, clause-wise manner, along with practical examples for better understanding.

Recent Updates

21st December 2024

In its 55th meeting, the GST Council proposed a key change to Section 17(5)(d) of the CGST Act.

- The term “plant or machinery” will be replaced with “plant and machinery”, and this change will apply retrospectively from 1st July 2017.

- This amendment ensures consistency with the explanation provided at the end of Section 17.

23rd July 2024

The Government of India also suggested further amendments to the blocked credit provisions under Section 17(5):

- Limit the restriction of ITC for taxes paid under Section 74 (related to fraud or willful misstatements) only for cases up to FY 2023–24.

- Eliminate references to Section 129 (detention/seizure of goods) and Section 130 (confiscation and penalty) from this provision.

Note: These changes will take effect once officially notified by the CBIC.

Overview of Section 17(5) of the CGST Act, 2017

Section 17(5) of the CGST Act outlines the rules for blocked credits, which refer to certain purchases or expenses where Input Tax Credit (ITC) is not permitted under GST. This means that even if GST is paid on these transactions, businesses cannot use it to offset their output tax liability.

The section contains 11 specific clauses that define situations where ITC cannot be claimed. Importantly, Section 17(5) takes precedence over the general ITC entitlement provided under Section 16(1) (which allows ITC for business-related use) and Section 18(1) (which deals with ITC in specific circumstances).

Claess used in specific businesses. This includes:

- Four-wheeled passenger vehicles (cars, SUVs, etc.)

- Three-wheelers (auto rickshaws)

- Two-wheelers (bikes, scooters, cycles)

- Tempo Travellers (TTs) or buses with up to 13 seats including the driver

- Any other vehicles designed for road transport

However, ITC can be claimed on such vehicles only if you are engaged in:

- Providing passenger transport services (e.g., cabs, taxis, buses)

- Renting or leasing motor vehicles

- Running driving training schools

- Operating an automobile dealership, showroom, or manufacturing unit

Clause (a) – Ships, Vessels & Aircraft

You are not eligible for ITC on GST paid for the purchase of ships, vessels, or aircraft, unless the business falls under one of these categories:

- Dealing in resale of such vessels or aircraft

- Providing transportation services (cruise liners, airlines, rental boats/planes)

- Running training institutions for ship navigation or pilot training

- Businesses engaged in goods transport via trucks, trailers, or tractors

Clause (ab) – Input Services Related to Conveyances

In addition to restrictions on claiming ITC for the purchase of vehicles, Input Tax Credit is also not available on GST paid for related input services, such as:

- Insurance premiums

- Repair and maintenance

- Servicing charges

…for passenger vehicles (like cabs, mini-buses, Tempo Travellers or buses with up to 13 seats), as well as ships, vessels, and aircraft.

Exceptions to Clause (ab)

Despite the restrictions, ITC is allowed on such input services if:

- Your business falls under the exceptions listed in Clause (a) (such as passenger transport, leasing, or training institutes)

- Your business meets the exceptions under Clause (aa) (like resale or commercial use of ships or aircraft)

- You are a manufacturer of these vehicles, vessels, or aircraft

- You are an insurance company offering general insurance policies for such conveyances

Clause (b) – Expenses on Food, Travel, Insurance, and Club Membership

Under Clause (b) of Section 17(5) of the CGST Act, businesses cannot claim Input Tax Credit (ITC) on GST paid for certain personal or employee-related expenditures, such as:

- Costs related to outdoor catering, meals, or beverages

- Spending on healthcare, beauty treatments, cosmetic or plastic surgeries

- Renting or leasing of vehicles, ships, or aircraft, except in cases covered under Clauses (a) or (aa)

- Premiums for life insurance or health insurance

- Charges paid for club memberships, health clubs, or fitness centres

- Leave Travel Concession (LTC) or vacation benefits provided to employees

When ITC Is Allowed

You may still be eligible to claim ITC in the following scenarios:

- If you’re reselling these goods or services

- If these items are sold as part of a composite or mixed supply

- If it’s legally mandatory for employers to provide such benefits to employees (e.g., as per labour laws or safety compliance)

Additionally, ITC is allowed for:

- Club memberships and travel benefits mandated by any law

- Telephone and broadband bills reimbursed for official business use

- Air travel undertaken by employees or directors for official purposes

- Accident insurance premiums for employees

- Canteen or refreshment services required under Factories Act, 1948 or other applicable laws

Important Clarifications for Employers

- No ITC is available on renting cabs for daily employee transport—unless required by law or if larger vehicles (with more than 13 seats) are hired for this purpose.

- Gifts given by an employer to employees are not eligible for ITC.

- Boarding and lodging expenses for employees on business trips are eligible for ITC.

- Perks that are part of the employee’s salary structure or contractual agreement do not attract GST, hence no ITC is involved.

Clauses (c) & (d) – Construction of Buildings

Under Clauses (c) and (d) of Section 17(5) of the CGST Act, a registered taxpayer cannot claim Input Tax Credit (ITC) on GST paid for the construction of buildings, whether used for residential or commercial purposes.

This restriction applies to:

- Construction work carried out on your own account

- GST paid on construction materials or services

- Renovation or repairs of buildings, if capitalised in the books of accounts

🚫 ITC is blocked regardless of whether the construction is for office use, business premises, or any other utility, if not for resale.

✅ Exception: ITC is allowed if the person is engaged in the sale of buildings post-construction, such as:

- Builders

- Real estate developers

- Promoters

Additionally, ITC is allowed for:

- Purchase or construction of plant and machinery

Clauses (e) & (f) – Composition Scheme & Non-Resident Taxpayers

Clause (e) of Section 17(5) bars composition dealers (as per Section 10 of CGST Act) from availing ITC. Since composition taxpayers pay a fixed tax rate on their turnover and do not collect tax from customers, they cannot claim ITC on inward supplies, whether goods or services.

Clause (f) restricts non-resident taxable persons from claiming ITC, except for IGST paid on imports. These taxpayers usually pay GST in advance, but ITC is not allowed on their local purchases within India.

Clause (g) – Personal Use of Goods and Services

Under Clause (g) of Section 17(5), Input Tax Credit (ITC) is not allowed for goods or services used for personal consumption. If the purchase is partly for business and partly for personal use, ITC can only be claimed on the business-related portion.

✔️ The allowable ITC should be calculated using the common credit apportionment formula provided under GST rules.

Clause (h) – Loss, Theft, and Free Distribution

As per Clause (h), ITC is disallowed on goods that are:

- Lost

- Stolen

- Damaged

- Written off

- Given away as free samples or gifts

🛑 Even if ITC was initially claimed during purchase, it must be reversed later in GSTR-3B if any of the above situations occur.

Clause (i) – ITC Claimed on Fraud or Misuse

Clause (i) restricts ITC in cases where tax is paid due to:

- Non-payment or underpayment of GST

- Excess ITC claimed or used

- Excess refund received

- Fraud, willful misstatements, or suppression of facts (for up to FY 2023–24)

🚨 This amendment is part of the proposed changes and will come into effect once notified by the CBIC.

❗ What If You Wrongfully Claim ITC under Section 17(5)?

If a taxpayer violates Section 17(5) and claims ineligible ITC:

- They must reverse the ITC

- Interest @ 24% per annum applies from the date of wrongful claim until reversal

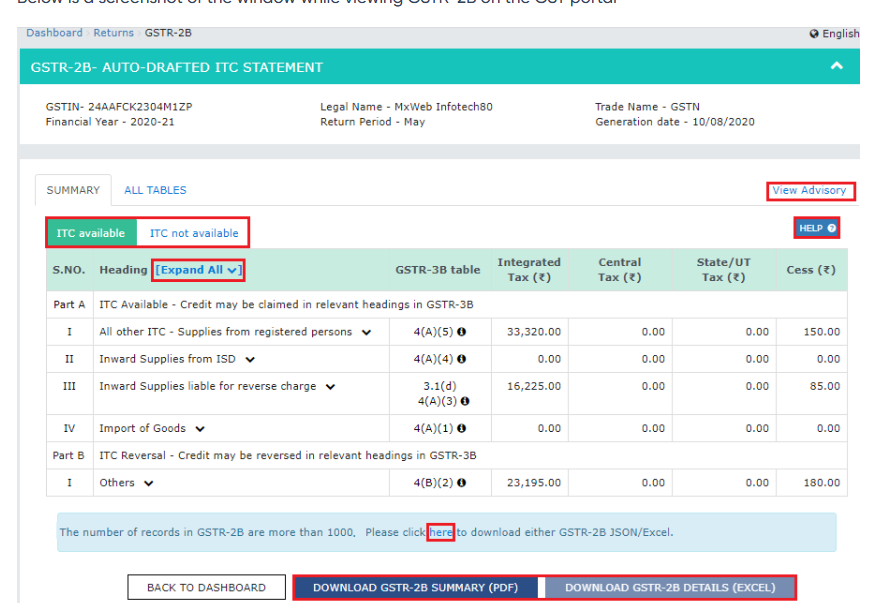

📄 How to Check Ineligible ITC Under Section 17(5)?

To view the list of ineligible ITC:

- Login to the GST portal

- Go to Returns Dashboard

- Access the GSTR-2B (Auto-drafted ITC Statement)

- Select the tax period (month and year)

- Download and review your eligible vs. ineligible credits

🧾 GSTR-2B clearly indicates the purchases on which ITC is blocked as per Section 17(5).

📋 Reporting Ineligible ITC under Section 17(5) in GSTR-3B

Every GST-registered buyer or recipient must report ineligible Input Tax Credit (ITC) that falls under Section 17(5) of the CGST Act while filing GSTR-3B for the applicable month or quarter.

✅ Where to Report?

From 5th July 2022 onwards:

- Table 4(B) of GSTR-3B must be used to report and reverse ineligible ITC under Section 17(5).

- Do not report the same in Table 4(D). Only Table 4(B) is required for this purpose.

🔍 Cross-Verification with GSTR-2B

To ensure accurate reporting:

- Compare your books of accounts with the ineligible ITC list in GSTR-2B (Auto-drafted ITC Statement).

- In your books, ensure that ITC is initially recorded at the time of purchase/expense entry but not added to the available ITC if it’s ineligible.

- If any ineligible ITC has been claimed mistakenly, reverse it in Table 4(B) of the next GSTR-3B, along with interest at 24% per annum from the date of incorrect claim.

📌 Key Point:

Regular reconciliation between GSTR-2B and books of accounts is essential to:

- Avoid wrongful ITC claims

- Ensure timely reversals of ineligible ITC

- Remain compliant with Section 17(5) and avoid penalties

🧾 FAQs on Section 17(5) of CGST Act & GSTR-3B Reporting

1. What is Section 17(5) of the CGST Act?

Section 17(5) lists specific goods and services on which Input Tax Credit (ITC) is not available, also called blocked credits. These include personal expenses, construction of immovable property, motor vehicles, and more.

2. Can ITC be claimed on food and catering expenses?

No, ITC on food, catering, and beverages is not allowed unless they are used for resale, as part of a composite/mixed supply, or are mandated by law to be provided to employees.

3. Is ITC available on motor vehicles?

ITC is not available on motor vehicles used for transporting passengers unless you are in the business of:

- Passenger transport

- Vehicle rental/leasing

- Driving schools

- Vehicle manufacturing or sale

4. Where should ineligible ITC be reported in GSTR-3B?

All ineligible ITC under Section 17(5) must be reported in Table 4(B) of GSTR-3B. Since 5th July 2022, it is not necessary to report it in Table 4(D).

5. What if ineligible ITC is wrongly claimed?

You must reverse the wrong ITC in the upcoming GSTR-3B and pay interest at 24% per annum from the date of incorrect claim until reversal.

6. How to identify ineligible ITC in GSTR-2B?

GSTR-2B classifies ITC as eligible and ineligible. You can log in to the GST portal, go to the return dashboard, and download GSTR-2B for the relevant period to review ineligible credits.

7. Can ITC be claimed on construction expenses?

No, ITC on goods/services used for construction of immovable property (when capitalised) is not allowed, except for plant and machinery or when used for resale by builders and promoters.

8. Is ITC allowed on health insurance and club memberships?

Generally, no. However, ITC is allowed if such services are:

- Made compulsory by law for employers to provide, or

- Part of a composite/mixed supply for resale

9. Can I claim ITC on lost or damaged goods?

No. ITC is not allowed on goods that are lost, stolen, destroyed, written off, or given as free samples or gifts.

10. What happens if I don’t reverse ineligible ITC?

Failing to reverse ineligible ITC can lead to:

- Recovery proceedings by GST authorities

- Interest at 24% per annum

- Penalty and prosecution in cases of fraud