The Income Tax Act includes provisions for tax deduction at source (TDS) on rent payments and payments related to joint development agreements. Section 194-IB focuses on TDS for rent, while Section 194-IC covers TDS for payments under a Joint Development Agreement (JDA) in real estate.

Updates from Budget 2024:

From October 1, 2024, the TDS rate for rent payments under Section 194-IB will be reduced from 5% to 2%.

Section 194-IB: Key Points

Section 194-IB applies to individuals or Hindu Undivided Families (HUFs) who are not required to get their accounts audited under Section 44AB. If they pay rent exceeding ₹50,000 per month to a resident, they must deduct TDS. Currently, the TDS rate is 5%, but it will drop to 2% starting from October 2024.

What is Considered as Rent?

Rent includes payments made under a lease, tenancy, or any similar arrangement for the use of:

- Land

- Buildings (including factory buildings)

- Machinery

- Furniture

- Equipment

- Plants

- Fittings

The person receiving the rent may or may not own the property or assets.

When to Deduct TDS Under Section 194-IB?

TDS should be deducted by the tenant at the earlier of these two events:

- When rent is credited to the landlord’s account (for the last month of the financial year or tenancy), or

- When rent is paid in cash, cheque, or other modes.

TDS Rate Under Section 194-IB

- 5% if rent exceeds ₹50,000 per month.

- 20% if the landlord’s PAN is not available.

Section 194-IC: Key Points

Section 194-IC deals with TDS on payments made under a Joint Development Agreement (JDA). A JDA is when a landowner allows a developer to construct a real estate project on their land in exchange for a share of the project or monetary compensation.

When to Deduct TDS Under Section 194-IC?

TDS should be deducted at the earlier of these two events:

- When income is credited to the landlord’s account, or

- When payment is made to the landlord.

TDS Rate Under Section 194-IC

The TDS rate under Section 194-IC is 10% for payments made to the landowner under the JDA.

Time Limits for Depositing TDS

For non-government payments:

- TDS must be deposited within seven days after the end of the month in which it was deducted, except for March payments, which are due by April 30. For government payments:

- TDS must be deposited on the same day it is deducted.

For Section 194-IB, the tenant must use Form 26QC to deposit TDS within 30 days from the end of the month when the deduction is made.

How to Pay TDS on Rent

Tenants must deduct TDS once per financial year, either in March or at the end of the tenancy. They must file a Form 26QC and issue Form 16C (a TDS certificate) to the landlord. A Tax Deduction Account Number (TAN) is not required for this process.

Penalties for Non-Compliance

If the tenant fails to deduct or deposit TDS on time:

- They may be penalized an amount equal to the unpaid TDS.

- Late payment of TDS can attract a 1% interest for delay in deduction and 1.5% for delay in deposit.

- Failure to file Form 26QC within 30 days will result in a late fee of ₹200 per day.

This simple breakdown should help tenants and developers understand their responsibilities under Sections 194-IB and 194-IC to avoid penalties and ensure timely compliance.

Online TDS Payment Procedure under 194-IB

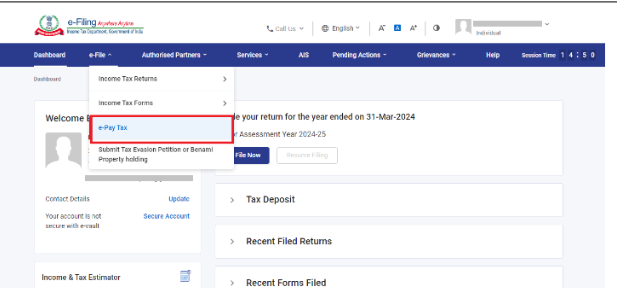

Step 1: Log in to your income tax portal.

Step 2: Once Logged in, Go to E-file >> E- Pay Tax.

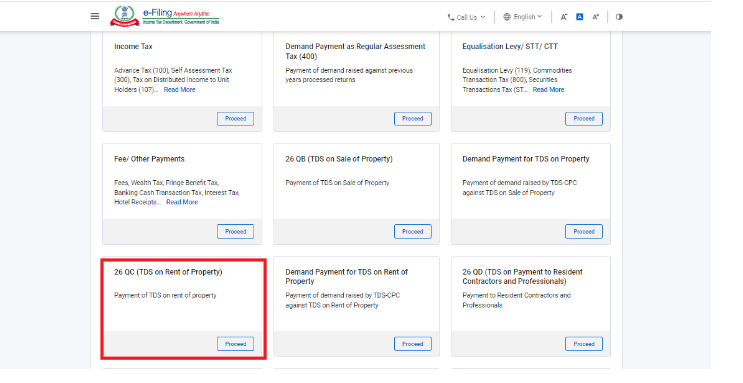

Step 3: Select on New Payment >> 26QC (TDS on Rent of Property)

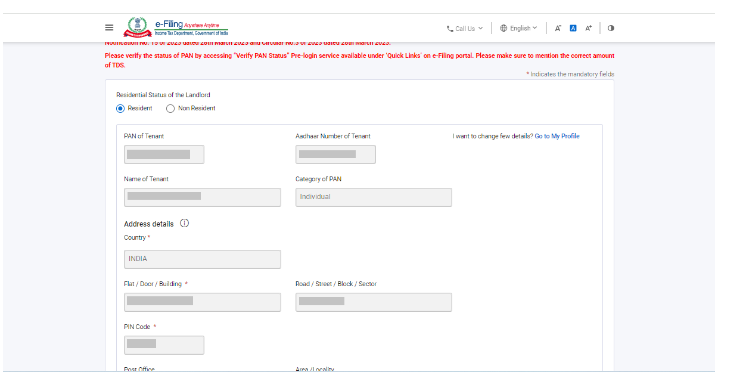

Step 4: Enter the tenant’s information, including the landlord’s PAN and address. Also, provide details about the rent being paid and the TDS deduction. Once you have filled in all the required information, proceed to make the tax payment.

Enter the tenancy period, rent amount, and any other relevant information.

Step 5: After submitting, make a note of the payment acknowledgment number for your records. You can download and print Form 26QC for documentation. Additionally, remember to give Form 16C to the landlord as proof of tax payment, which they can use when filing their taxes.

Frequently Asked Questions

When should TDS under Section 194-IB be deducted?

TDS under Section 194-IB applies to individuals and HUFs paying rent exceeding ₹50,000 (those not covered under Section 194I). This TDS should be deducted in March and must be remitted or filed by the 30th of the following month, i.e., by April 30th.

I am a salaried individual paying ₹60,000 per month in rent for my accommodation. Am I required to deduct TDS under Section 194-IB?

Yes, every resident individual paying rent of more than ₹50,000 per month is obligated to deduct TDS under Section 194-IB.

Is there any exemption from TDS under Section 194-IB?

TDS under Section 194-IB is applicable only if the rent exceeds ₹50,000 per month. If your rent is less than this amount, you are not required to deduct TDS or file Form 26QC.

What is the TDS rate for Section 194-IC?

For any payment made under the specified agreement (Joint Development Agreement or JDA), the person making the payment must deduct TDS at a rate of 10%.

How do I deduct TDS under Section 194-IB?

TDS under Section 194-IB is applicable on rent paid by individuals or HUFs exceeding ₹50,000 per month. This TDS should be deducted in March of the financial year and paid by April 30th.

What happens if the tenant does not deduct TDS?

If a tenant, who is an individual or HUF, fails to deduct TDS while paying rent exceeding ₹50,000 per month, they will be liable for interest at a rate of 1% per month on the unpaid TDS amount, as well as a penalty of ₹200 per day for late filing of Form 26QC.