An Income Tax Return (ITR) is a form that allows a taxpayer to report their income, expenses, tax deductions, investments, and taxes. According to the Income-tax Act of 1961, it is required for a taxpayer to file an income tax return in certain situations.

E-filing is the process of submitting an Income Tax Return (ITR) online. By logging into the new income tax portal with their PAN-based credentials, individuals can access features that make the tax filing process easier.

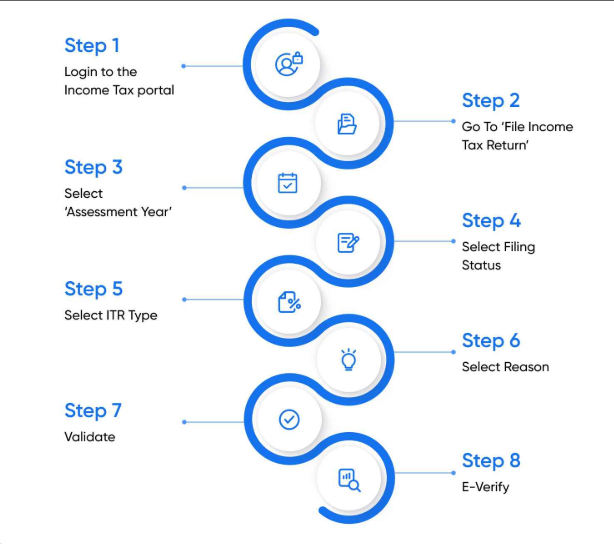

In this article, we’ll explain how to file your ITR in 8 simple steps!

Steps to E-file ITR on the Income Tax Portal

Step 1: Login

Go to the Income Tax Portal and log in using your PAN (which serves as your User ID), your password, and the captcha code.

Step 2: Go to ‘File Income Tax Return’

Click on the ‘e-File’ tab, then select ‘Income Tax Returns,’ and finally click on ‘File Income Tax Return.’

Step 3: Choose the Correct ‘Assessment Year’

If you’re filing for FY 2024-25, select ‘Assessment Year’ as ‘AY 2025-26.’

Make sure to choose the right filing type: original return or revised return.

Step 4: Choose Your Filing Status

Select the filing status that applies to you: Individual, HUF, or Others.

For most people, select ‘Individual’ and then click ‘Continue’.

Step 5: Choose the ITR Form

Before filing returns, the taxpayer needs to determine which ITR form they should use.

There are 7 different ITR forms, and ITR 1 to 4 are for Individuals and Hindu Undivided Families (HUFs).

For example, if an individual or HUF has capital gains but no income from business or profession, they should use ITR 2.

Step 6: Select the Reason for Filing ITR

In this step, you will need to choose the reason for filing your tax return. Select the option that applies to your situation:

- Your taxable income is above the basic exemption limit

- You meet specific criteria and are required to file ITR

- Other reasons

Step 7: Verify Pre-filled Information

Many of your personal details, like your PAN, Aadhaar, name, date of birth, contact details, and bank information, will be automatically filled in. Check these details carefully before moving forward.

You will also need to provide your bank account information. If you’ve already entered this, make sure it’s correctly pre-validated.

As you go through the steps, make sure to report all your income, exemptions, and deductions.

Most of the information will be pre-filled based on data from your employer, bank, etc. Double-check everything to ensure it’s accurate.

Finally, review your tax return summary, confirm the details, and pay any outstanding taxes if needed.

Step 8: E-Verify Your Income Tax Return (ITR)

The final and most important step is to verify your return within 30 days. If you don’t verify it, it’s like not filing it at all.

You can e-verify your return using various methods, such as Aadhaar OTP, electronic verification code (EVC), Net Banking, or by sending a signed physical copy of ITR-V to CPC, Bengaluru.

Why is Filing Income Tax Return Important?

The Income Tax Department requires individuals to file their return if their income is above the basic exemption limit or if they meet certain criteria. For example, if they spend more than Rs. 2 lakh on foreign travel, have electricity bills over Rs. 1 lakh, or deposit more than Rs. 1 crore in one or more current accounts in FY 2019-20 or later.

ITR filing is also mandatory if business receipts exceed Rs. 60 lakhs, professional receipts exceed Rs. 10 lakhs, or if TDS/TCS amounts exceed Rs. 25,000.

Even if you’re not required to file, it’s a good idea to file your ITR if you have overseas assets or accounts, as it provides several benefits.

Reasons to File ITR

- It acts as a valid proof of your income or net worth.

- You’ll need ITR for applying for loans in the future.

- It’s required by banks to apply for credit cards.

- It’s required for visa applications.

- It’s necessary to obtain term insurance.

- It’s needed for government tenders.

Therefore, even if your income is below the basic exemption limit, it’s still a good idea to file your ITR.

Documents Required for Filing ITR

Here are the documents/information needed to e-file your ITR:

- PAN and Aadhaar

- Bank Statements

- Form 16

- Donation receipts

- Stock trading statements from the broker platform

- Insurance policy receipts for life and health

- Bank account details linked to PAN

- Aadhaar-registered mobile number for e-verifying the return

- Interest certificates from banks

However, you can e-file your ITR easily by just entering your PAN. Most of your details, like salary income, TDS, and deduction information, will be auto-filled from the Income Tax Department.

How to Download an Income Tax Return (ITR) Copy Online

Step 1: Visit incometaxindiaefiling.gov.in and log in using your credentials.

Step 2: Navigate to the “View Returns/Form” section.

Step 3: Select “Income Tax Returns,” choose the relevant assessment year, and click “Submit.”

Step 4: A list of your filed ITRs will be displayed.

Step 5: Click on the ITR-V acknowledgment number for the return you wish to download.

Step 6: The ITR-V form will open in PDF format, which you can download and save.

Frequently Asked Questions

1. How can I pay income tax online?

You can pay your income tax either online or offline. For detailed instructions, please refer to this guide [insert link].

2. How is income tax paid to the government?

Income tax must be paid before filing your tax return. If you are a salaried employee, your employer typically deducts Tax Deducted at Source (TDS) from your salary and deposits it with the government on your behalf.

If you are required to pay advance tax, ensure that at least 90% of your liability is cleared by March 31st of the financial year.

3. How can I file an income tax return after the due date?

The deadline to file your Income Tax Return (ITR) is July 31st. If you miss this date, you can still file a belated or updated return. However, late filing fees, interest, and additional penalties (in case of updated returns) may apply.

4. How do I file an income tax return for previous years?

You can file returns for previous years using the updated return form (ITR-U). Note that there are certain conditions and limits regarding which years you can update. For more detailed information, please see this article [insert link].

5. How can I check if my ITR has been filed?

- Step 1: Log in to the income tax e-filing portal using your user ID and password.

- Step 2: Navigate to e-File > Income Tax Returns > View Filed Returns.

- Step 3: Review your filed returns. You can filter the view by Assessment Year or Filing Type. Click “View Details” to check the status and action items (e.g., pending e-Verification).

Note: If your PAN is not linked with Aadhaar, it may cause delays, including refund holds.

6. What if I missed the due date or made a mistake while filing my ITR?

- Missed the Due Date: You can file a belated return by December 31st of the assessment year. For FY 2024-25 (AY 2025-26), the last date is December 31, 2025. A late filing fee under Section 234F will be applicable.

- Made a Mistake: You can revise your filed ITR by December 31st of the assessment year.

- Missed Both Deadlines: You may still file an Updated Return (ITR-U) if eligible, subject to additional conditions and penalties.

7. When will I receive my income tax refund?

Typically, it takes between 30 to 90 days after filing for your refund to be processed. You can track your refund status [insert link].

8. Is it necessary to submit documents while e-filing the ITR?

No documents need to be attached while e-filing. However, it is advisable to retain all relevant records, as the tax department may request them during an assessment.

9. What happens if I do not e-verify my income tax return?

You must e-verify your return or send a signed physical copy to the CPC in Bengaluru within 30 days of filing. Failure to do so will render your return invalid, meaning it will be treated as if it was never filed.

If e-verification happens after 30 days:

- The filing date is considered the date of verification.

- Late filing fees of ₹5,000 or ₹1,000 may apply.

The return will be processed under the default tax regime, even if you had opted for the old regime, and ineligible exemptions or deductions will be disallowed.